.jpg)

What can your entity do for you?

- Jan 31, 2019

- 3 min read

What can your entity do for you?

There are many types of entities. Of course each entity has PURPOSE and boundaries which may be unique to that entity. In addition, often there are synergies between entities and strategies making each one more powerful when used with another. Regardless of which entity is used, the entity should be used for your purpose both short term as well as long term.

This is not to say one entity is always better than the other, however one entity may allow you to accomplish your objective more effectively than another. In addition, there is synergy while combining multiple entities to accomplish either specific purposes or general purposes. The benefits expand from simply running a business, to asset protection, capital preservation, taxation, ownership, transfer of assets, future sell or gifting, philanthropy, etc. These decisions affect the business owner, partners, employees, key employees, as well as future generations.

Here are some key questions to ask about your current and future entities:

What is my objective?

What are the restrictions of this entity?

What are the boundaries?

What are the Benefits and or Liabilities?

How is it taxed?

Is it flexible?

What is the Ownership?

Begin with the Exit in mind?

Each of these questions should be asked in the context of both short term and long term planning. Here are a few of the entities that every business owner should consider:

LLC. An LLC provides a level of legal protection, along with tremendous flexibility. A business owner has the flexibility to be taxed either as an S Corp or a C Corp, a partnership or a disregarded entity.

Partnership. A partnership is a legal form of business operation between two or more individuals who share management and profits. The federal government recognizes several types of partnerships. The two most common are general and limited partnerships. Partnerships are the most flexible structures and provide tax efficiency including non-qualified, incentive based plans for executives and key employees.

S Corp. The advantages in the past included being a flow through for tax purposes. This still may be the case, however many business owners are structured this way when another option may be more efficient and beneficial to their purpose.

C Corp. Traditionally, many business owners have shied away from this entity because of “double taxation.” This may be the case, but where dividends are not contemplated, the 35% corporate tax rates represent a 5% savings over flow through entities, and also benefit from Tax free dividends to/from other C Corps, and other benefits.

QSBS (Qualified small business stock) sometimes referred to as 1202, is an election that some qualified C Corps may elect which puts them in position for a Tax Free exit. Boundaries include what type of business, what size of business, and the timing and type of future sale of the business. When a qualified small business sells, the outcome is significant and Tax Free, specifically the greater of ten times basis, or $10 million. Proceeds from a sale also can be utilized similarly to a 1031 exchange.

Trusts. The diversity of trusts, asset protection, philanthropic, estate and gift tax efficiency, and succession planning require the expertise of legal counsel. Charitable trusts, revocable trusts, irrevocable trusts, generation skipping trusts each have unique purpose. If one trust could do “it” all, there would be just one.

CRUT. Charitable remainder uni-trust. This particular type of trust is an entity serving multiple purposes and is created with real estate sale or pending sale of a business is anticipated. Benefits include philanthropy, lifetime income, tax deductions and tax deferral.

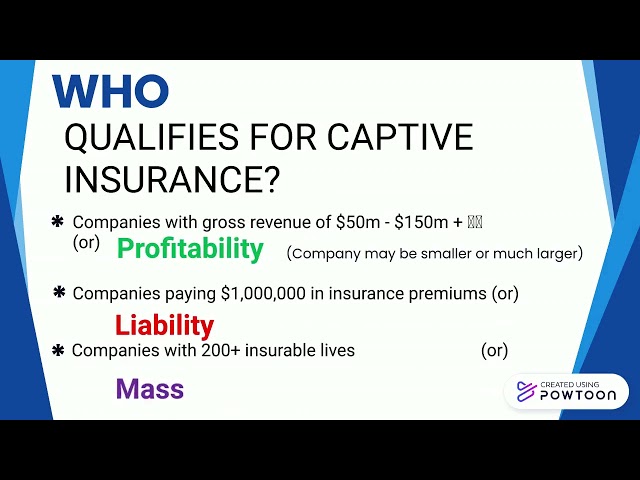

CIC. Captive Insurance Company. First, last and always the purpose of this entity is insurance. As an insurance company the CIC must be structured as a C Corp. Over time, the flexibility of this entity is unmatched. This entity is the catalyst when working with additional entities while protecting the operating company.

ESOP An employee stock ownership plan allows the owners to sell stock of their company, typically a C Corp, to their employees, either partially or fully and both the owners and the employees benefit. The owners profit immediately through tax efficiency of Tax Free proceeds and proper tax deductions. There are multiple additional benefits, including employee retirement, as well as continued control of the operating business.

Disclaimer. Please consult your qualified accountant or legal counsel regarding proper structuring of these entities. Not all businesses qualify for potential use of these entities, and not all accountants and legal counsel are familiar with these entities as well.

Note: ALINK works with these qualified experts in each of these areas, specifically Goodspeed & Merrill and third party administrators who specialize in the listed entities.

Your Link to Security!

Rich Ericson, President Nathan S. Merrill

ALINK Captive Insurance Services Main: 720-473-7644

• Direct: 720-213-0583 Ph: 720-515-1121

• Email: Rich@ALINKcis.com Fax: 720-473-7647

Comments