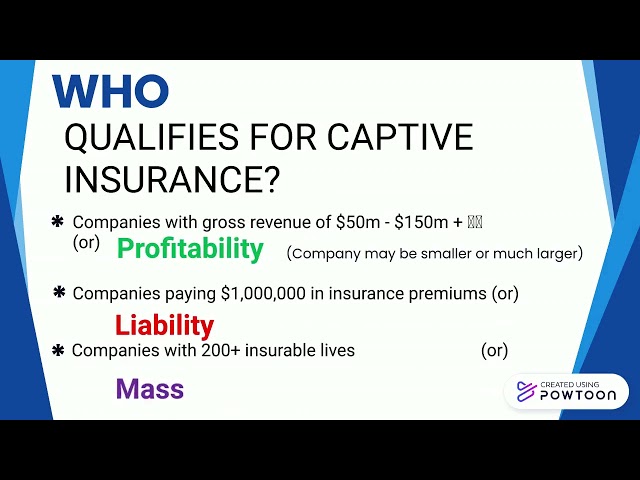

.jpg)

Specific Captive Risks

- Feb 28, 2020

- 3 min read

What does insurance really look like? A photograph of your 2017 Mercedes, book value and all are easily noted, your home insurance likewise. As a business owner, underwriters can review your financials and the appropriate amount of life insurance can be written. How much would it cost you and your business to replace your key employee? How much time and expense would be involved if your technology, data, were not accessible and breached?

There are more than 75 risks covered through Captive Insurance policies. These risks are determined by actuaries, who specialize in underwriting risks. These exposures are underwritten and re-insured through the captive manager. The business owner chooses the risks most important to him or her, and has the ability to change or adjust exposures at renewal, as different exposures take on a higher priority for them.

Risks often are broken down into a variety of categories like strategic, operational or core risks. Another way to view these risks are broad or very specific. An example of this is business interruption which could include multiple events to very specific risks like loss of a license, or directors and officer coverage.

Another example of a broad risk – Loss of Key Customer. This type of exposure is insurable as long as the loss of the key customer was the result of some event beyond the control of the Company. The risks that a contract will be wrongfully cancelled, or that the key customer suffers financial setbacks, and must file for bankruptcy, hence causing the contract to be voided. Moreover, a loss of a key customer would likely take two to three years to replace and cost the Company loss of internal time and revenue. Insurance for Loss of Key Customer is typically not available in the commercial marketplace, but can be insured in a captive, but only to the extent the exposure applies.

Here is an example of some specific risks - Failure to perform on contract. Contract Penalty and Failure to Perform on Contract could be legitimate risks to the Company. Based on the information presented, in the event The Company is awarded a contract and does not meet contractual obligations, payment would likely be withheld and potential damages could be assessed, which would have an impact on net income. This type of coverage may not be readily available in the marketplace, thus making it appropriate for a captive insurance program.

Reputational Risk. Reputational Risk, as the term is used in the commercial insurance market, is an exposure a company has to its perceived reputation. It concerns the risk that negative publicity regarding an institution's business practices will lead to a loss of revenue or increased litigation. An institution's reputation, particularly the trust placed in the organization by its customers, may be irrevocably blemished due to perceived or actual breaches in its ability to conduct business ethically, securely, and responsibly. That reputation can be impaired by a variety of events, whether criminally intentional, or merely unfortunate and inadvertent. Adverse events typically associated with reputation risk include matters of ethics, safety, security, sustainability, quality, and innovation.

Most, if not all Companies are interested in maintaining a positive reputation in its market. The value placed on the Company’s reputation is a critical component to procuring and maintaining successful business relationships that directly impact net income. This risk can reasonably be insured through alternative risk financing strategies, but business owners should review any captive policy language carefully to understand its applicability.

What’s your risk? Not insuring “it”, or continuing to informally self- insure these risks. Through YOUR Captive Insurance Company you formally provide coverage for these risks. Your Captive is Your Link to Security!

Rich Ericson, President

ALINK Captive Insurance Services

• Direct: 720-213-0583 • Email: Rich@ALINKcis.com

Comments