.jpg)

What's the Risk? Financed Life Insurance

- May 7, 2019

- 3 min read

We face many risks each and every day of our lives. It seems as though there is insurance for nearly all of them including mortality risk. We can delay it, prepare for it, work to prevent it, yet the fact remains we cannot avoid our future death. Whether or not a person insures against this future loss and the right policy for them, is certainly their prerogative.

At ALINK Captive Insurance Services, we specialize in risk management: the practice of appraising and controlling risk using various strategies.

Have you ever purchased a home using a mortgage? Knowing that it would take the average person many years to save up enough money to pay cash for a home, financing it makes sense to maintain cash-flow, so we can continue living life while also building equity in our own homes. While it may sometimes seem risky to finance a large sum of money, using a lender’s funds still makes the best sense, if the property you are purchasing is a good investment. High net worth individuals have learned there isn’t much risk to purchasing a second home or entering into a real-estate venture, because they have prior experience purchasing real estate, and they understand the benefits of using other people’s (lender’s) money to buy the things they need, safely.

Nearly everyone I speak with understands the purpose of life insurance. The best type of life insurance for each of us depends on the purpose and assets available to fund the insurance. High net worth individuals have a greater need for life insurance than most to protect their families, business and their wealth. That said, most successful people actively look for investment opportunities yielding returns greater than the cost of capital, and many need life insurance to address inheritance, business, and future estate tax issues, yet they would prefer to keep the funds they would spend on traditional life insurance premiums to utilize for additional money-making opportunities. Have you ever heard of financing insurance premiums?”

Life insurance reduces risk of estate taxation when you die. It reduces risk of your family not having assets to live on if you die. It reduces the risk of rising tax rates in the future. Financing the premiums allows the owner to utilize his or her assets more effectively. Permanent life insurance creates an additional asset to access while you are very much alive. As you become familiar with financed life insurance and the controllable variables involved you will see how ALINK Captive Insurance Services utilizes the best contracts, companies, and lenders to reduce or eliminate any inherent risks of the policies or lenders.

As an example:

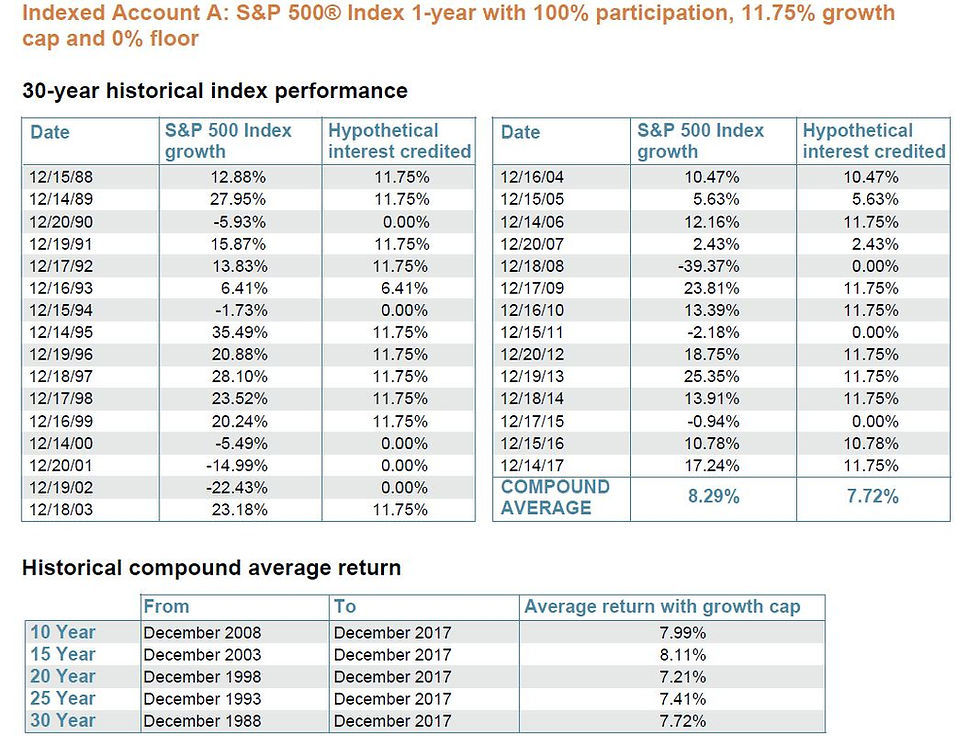

Policies have an investment floor of 0%. You will not lose money due to market volatility.

Policies have a cap of 11.75%.

We have looked at every scenario in the history of our country. These policies have always averaged around 7%.

Policies are illustrated using historical average rate of returns. Based on historical averages over multiple periods since 1988, the likelihood of an average return lower than 6% is very low.

*Minnesota Life illustration and historical averages data above from July 2018.

Remember, the policy is not going to return 7% every year. It could be less. It could be more. The data provided shows there is typically a positive return every year of no less than 0% and no more than 11.75%, in other words, these policies have historically averaged close to 7%. Financed life insurance is a long-term strategy.

So, is it risky? History says it’s not.

Let me show you how it works and how to create

Your Link to your Security!

Rich Ericson, President

Alink Captive Insurance Services

• Direct: 720-213-0583 • Email: Rich@AlinkCIS.com

Comments